Implementation of Transport Biofuels Policies

Full title of the report: “Implementation Agendas: Compare-and-Contrast Transport Biofuels Policies (2019-2021 Update)”

Implementation Agendas: Compare-and-Contrast Transport Biofuels Policies (2019-2021 Update)

IEA Bioenergy Task 39 (Transport Biofuels) has been assessing the measures taken by its member countries to develop or stimulate their respective biofuels sectors since 2007, with the particular focus on biofuel policies. The overall goal of this assessment was to determine the extent to which policies had been effective in encouraging the production and use of transport biofuels. Task 39’s member countries represent a diverse range of regions, biofuels producers and consumers and include some of the key biofuel producing countries and regions in the world (e.g., US, Brazil, Europe). This frequent assessment has been a central part of Task 39’s commitment to facilitate the commercialisation of low-carbon intensive transport biofuels. The increasing global production and use of biofuels plus the growing numbers of national and regional policies that support the development of biofuels markets to decarbonize the transport sector have been key components of the sector growth. Five updates of the report have been published by Task 39 in the past including 2007, 2009, 2014, 2017 and 2019. This recent update describes ongoing developments in the biofuels sector and the successful policies used by member countries to facilitate the production and use of low-carbon-intensive biofuels.

Analysed countries/regions are: Australia, Austria, Brazil, Canada, Denmark, European Union, Germany, India, Ireland, Japan, Netherlands, New Zealand, Norway, South Korea, Sweden, and the United States.

The main “takeaway” messages from the 2019-2021 triennium update are:

- Biofuels continue to be a central component to decarbonize the transport sector. Despite a trend towards greater electrification of road transport, biofuels (mainly ethanol and biodiesel) account for more than 90% of renewable energy in the transport sector and remain central to many national and sub-national renewable transport policy frameworks.

- Globally, biofuels production continues to increase. In the vast majority of member countries, biofuel policies have enhanced biofuels market growth. Biofuel policies will continue to play an essential role in the growth of biofuels market.

- “Conventional” biofuels (i.e. ethanol/biodiesel) continue to dominate the market but the production and use of drop-in and advanced biofuels (i.e. renewable diesel) has been growing rapidly. Low-carbon intensive fuels can also be produced by co-processing biogenic feeds in existing oil refineries.

- Despite considerable progress being made in the technical aspects of advanced biofuels production, it is widely recognized that the right policies will be needed to help expand commercialization.

- Technology-push policies typically help drive early-stage development such as research and development (R&D), demonstration and commercialization of biofuels. These types of policies are used to help reduce the cost/risk of R&D and help take early-stage technologies through the financial “valley of death” that exists between initial development and commercialization. Market-pull policies (such as blending mandates; fuel and CO2 excise reduction or exemptions) are used to support technologies that are relatively mature and help create a demand for biofuels. Despite the predominance of market-pull policies, technology-push policies have been successfully used to encourage research, development and demonstration, particularly for advanced biofuels. A combination of technology-push and demand-pull policies will both be needed to increase the rate of introduction and diffusion of advanced biofuel technologies. The countries that have achieved the most success in growing the production and use of transport biofuels have used a mixture of market-pull and technology-push policies.

- Biofuel blending mandates remain one of the most widely adopted mechanisms for increasing biofuels use in the transport sector. However, biofuel mandates alone have not always provided sufficiently strong incentives to spur producers to continue to innovate and reduce the carbon intensity of the biofuels they produce.

- As well as encouraging on-going more efficient production of conventional biofuels, Low carbon fuel standard (LCFS) and the GHG emission quotas have proven to be a successful policy instrument to stimulate the development and production of lower carbon intensity drop-in and advanced biofuels by increasing their market values.

- As LCFS type policies become more common in increasing numbers of jurisdictions, the carbon intensity of current and emerging biofuels is expected to decrease.

- Most of the policies that have been used to promote renewable energy for transport have primarily focussed on road transport at a national level. Other important transport sectors such as aviation and shipping have received considerably less policy attention despite being significant energy consumers and carbon emitters. Regulators need to create a framework that mandates the use of low carbon fuels and incentivize production of biofuels for use in the aviation and shipping sectors.

- Sustainability requirements are increasingly being incorporated into biofuels policies, with LCFS type policies that incentivize reductions in carbon intensity and assure sustainability increasingly being used.

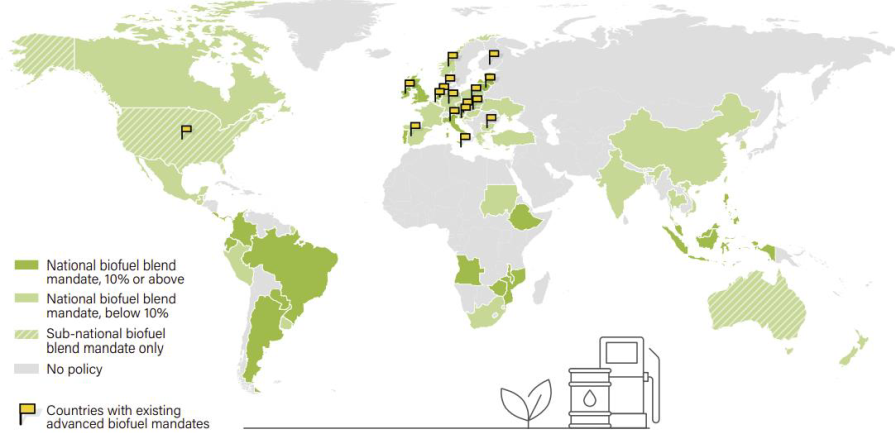

National and sub-national renewable transport mandates, as of end-2019 (Source: REN21 Policy Database, REN21, 2021)