Renewable Gas – discussion on the state of the industry and its future in a decarbonised world

This report is produced by members of IEA Bioenergy Task 37 (energy from biogas) to discuss the state of renewable gas and its future in a decarbonized world.

Decarbonisation is about so much more than electricity; electricity itself only accounts for about 20% of final energy demand. As a society we must make decisions informed by scientists and engineers and implemented through policy as to what technologies and roadmaps will be employed to decarbonise the hard to abate sectors including for: heavy transport; high temperature industrial heat; agriculture; fertiliser and chemical production. When it is considered that at present in the EU and the USA, the natural gas grid provides considerably more energy than the electricity grid, it cannot be seen as a sensible process to abandon such infrastructure and start again, not with the imminent climate emergency and the need to act fast. We must be decisive as we eat through our ever-dwindling allocated carbon budget to limit world temperature rise to below 2°C.

The existing natural gas infrastructure is very extensive in many industrialised countries and rather than being viewed as a future redundancy associated with a fossil fuel system, it could instead be seen as offering huge benefits for green renewable gas as a future decarbonised energy carrier. The whole natural gas infrastructure system was put in place at huge cost and includes for an extensive transport system of transmission and distribution pipes and connections to industries and homes. Within specific industries, gas boilers, CHP units and associated systems are in place to provide the necessary ingredients and energy provision for end products that range from ammonia to whiskey.

Traditional renewable gas technologies (such as biogas and biomethane) can be considered mature. We have the technologies in place to make renewable gases from wet organic material, dry woody material and from electricity. In southern Sweden for example biomethane is used extensively as a transport fuel in buses, trucks, and cars. We already inject biomethane to the gas grid. For example, Denmark has at times substituted natural gas in the grid with over 25% biomethane; these values fluctuate over the year. In terms of policy, we have devised and put in place trading mechanisms for trade between producer and user of renewable gas, sometimes in different countries.

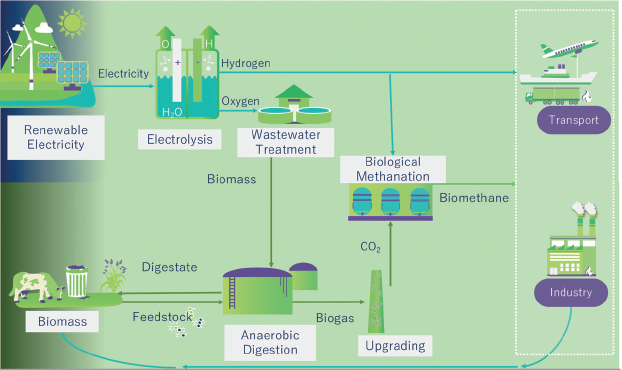

Figure: combining anaerobic digestion and electrolysis to maximize biomethane production

Figure: combining anaerobic digestion and electrolysis to maximize biomethane production

The economic feasibility of renewable gas is often questioned; however, this is a green fuel which is being compared to a fossil fuel where the climate cost of fossil carbon is in no way taken into account. As such, it is preferable to contrast the cost of renewable technologies with the cost of other renewable technologies which are viable in that sector; for example, we should not compare the cost of abatement of mature technologies in readily decarbonised sectors (say PV arrays) with that of an advanced transport fuel that can power heavy transport. We need to incentivise technologies at early market maturity and at low technology readiness levels (TRL) that are seen to have great potential for application as fuels of the future for hard to abate sectors such as hydrogen and associated electro-fuels.

At present however, the main barrier to uptake in the market for renewable gas is the cost. Future support systems and development strategies and policy must create conditions to integrate renewable gases into a new climate neutral economy. Whilst incentives are required at present to compete with fossil fuels, a strategy on the role renewable gas plays in the future market must be devised. Sustainable renewable gaseous fuels will be required to substitute for the huge market in place which uses natural gas and upcoming demand in new energy systems. In particular, attention must be paid to the existing natural gas infrastructure and how this massive capital investment could be capitalised upon.

In this report, the following actions have been identified to optimise the future development of renewable gas systems:

- Create roadmaps for renewable gas development, including for availability of substrates (be they wet organic, woody or electricity), development costs, defined time specific targets as a portion of energy use and infrastructure required and/or already available.

- Introduce quotas which place an obligation on fuel providers to ensure renewable fuels meet a minimum proportion of the fuel market; this is a very effective tool to remove the necessity of renewable gas competing on price with fossil gas.

- Provide incentives which reflect the actual costs of investment and long-term operation of the renewable gas industry to ensure bankability for the developer and ensure a price effective market environment for the user of renewable gas.

- Eradicate as much as plausible, unnecessary barriers and inhibitory regulations on both a technical and regulatory level.

- Seek compatibility and synergies with other technologies (both existing and proposed) through a cascading approach to further develop the sector; this could include for example carbon capture from industry combined with hydrogen from electricity to produce methane, methanol or ammonia in electro-fuel systems.

- CO2 emissions must have a realistic monetary value associated with them; a realistic carbon tax would stimulate development and drive the transformation of green gas whilst providing for competition between renewable technologies in specific sectors, which should consequently lead to the phase out of specific incentives.

Citation: Liebetrau, J., Rensberg, N., Maguire, D., Archer, D., Wall, D., Murphy, J.D. (2021) Renewable Gas – discussion on the state of the industry and its future in a decarbonised world, Murphy, J.D. (Ed.) IEA Bioenergy Task 37, 2021:11.

Full report: Renewable Gas Report_END

Short summary: 2-page summary-Renewable Gas Report